Cash App, the peer-to-peer financial technology application owned by Jack Dorsey’s Block, has introduced a new “pay-over-time” deferred payment option enabling qualifying users to spread their everyday transfers over an extended timeframe.

More companies are increasingly providing deferred payment options for standard and routine purchases. Approximately a year ago, DoorDash collaborated with Klarna—enabling users to “micro-finance” their meal orders (the collaboration notably led to a wave of online humor about “burrito debt” and late capitalism). Cash App’s latest feature clearly capitalizes on this trend—broadening convenient financing into the P2P payment sector.

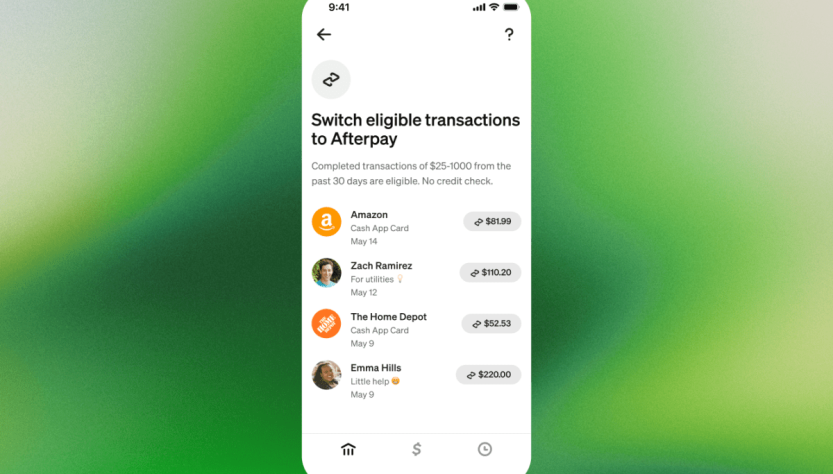

To benefit from this new feature, users incur a 7.5% fee—indicating that if you borrow $100 from Cash App, your repayment to the company will total $107.50. The company states transfers of $25 or more qualify, with repayments possible in weekly installments over up to six weeks or as a lump sum on the due date.

There are also loan thresholds in the new system, which are variable—implying they will differ among various users. “The precise amount eligible for conversion depends on the initial transaction amount and customer assessment,” a representative stated. “We assess each transaction for eligibility according to our responsible lending standards rather than establishing conventional credit thresholds,” they further noted.

In a discussion, Block’s Executive Officer and Head of Business, Owen Jennings, positioned the new feature as a method to enhance value for Cash App users through “cash flow management.” Jennings pointed out that numerous Americans today have different types of jobs—many of which pay with less regularity than those available in earlier decades. The aim of Cash App’s new feature is to provide financial adaptability to these circumstances, Jennings explained.

“We’re observing a growing number of individuals—especially younger ones—who are solo-preneurs, entrepreneurs… [and] gig workers. They engage in side hustles, juggling multiple positions, [and] thus possess fluctuating income sources,” Jennings stated. “This significantly contrasts with the situation 40 or 50 years ago—where the average income earner in the U.S. was typically receiving a regular W2 income biweekly.”

“Buy now, pay later” solutions have surged in popularity in recent years while also provoking major criticism and concern. Some critics argue that such services are constructed to ensnare consumers in continual debt cycles, whereas others imply that Americans’ need to finance basic household goods signifies a broader economic crisis. Firms offering these services have similarly encountered legal issues. Just this week, Klarna faced a class-action lawsuit alleging it engaged in “predatory” practices, according to Bloomberg.

Techcrunch event

San Francisco, CA

|

October 13-15, 2026

Jennings mentioned that Cash App’s new feature includes robust built-in safeguards designed to keep users from falling into financial difficulties, such as being caught in what he termed “debt spirals.” “All of our lending products are designed to be non-revolving,” he remarked. “If you fail to repay a loan, you will not be able to obtain another loan.”

The service also leverages existing financial flexibility features that Cash App already provides, Jennings noted. In previous years, the app launched Borrow, which similarly to a conventional bank, enables users to secure a small loan from the app and repay it over a period of four to six weeks.

Another offering is Afterpay for Cash App Card (its debit program), which permits users to postpone payments for transactions made using the card.